Data Science in Strengthening Debt Management Processes

Futurism Technologies

April 15, 2019 - 4.2K 5 Min Read

The global credit environment absorbed the effects of the financial crisis at varying speeds. In some places, loss rates have remained relatively high, in others, the past decade has seen steady improvement, with tapering losses that have only recently begun to climb again. With global expansion, markets lenders have increased their risk exposure by issuing newer products designed around easier underwriting guidelines. In a bid to chase numbers, little attention has been paid on maintaining and improving collection ability – resulting in debt load rise. With a highly stressed market where the convention skills and staff don’t work, there is a need for more efficient and effective collection operations.

Data Science has become the most dominant theme across all industries. The banking industry is no stranger to benefits of advanced analytics, across a wide array of sub-verticals like lending, regulatory, personal finance, insurance, wealth management, and debt management. There are various applications of advanced analytics which are helping banks to make better business decisions and improve profitability.

The need to renew collection operations provides lenders an ideal opportunity to build new technologies. The need to enable collection operation using advanced analytics and machine learning is the need of the hour. These powerful digital innovations are transforming collection operations, helping to improve the performance at a lower cost. Moreover, better criteria for customer segmentation and more effective contract strategies can significantly improve performance for the collection operations. More accurate loss forecasting strategies with better customer segmentation result in a better performing collection process.

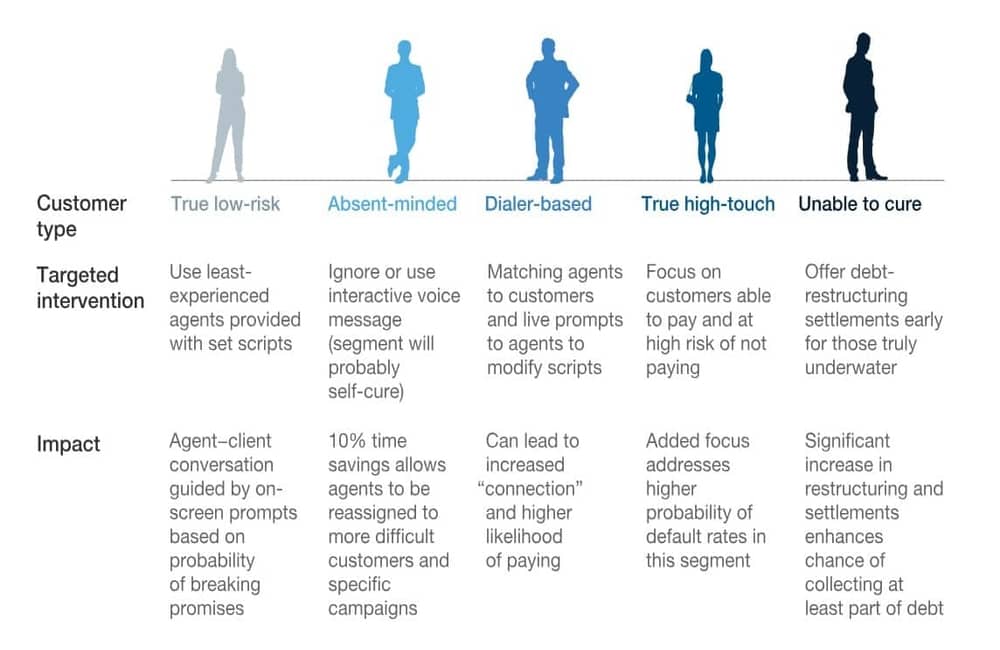

The traditional collection process segregates customers into a few simple risk categories, based on delinquency or simple analytics assigns to customer service teams. Lower risk customers are generally assigned to newer agents which follow a standardized script without evaluating customer behavior. The medium risk customers are assigned to agents with moderate skills set who follow a standardized script and are trained to assess customer behavior. Higher risk customers are assigned to skilled agents who use less standardized approaches to assess customer behavior.

The advanced analytics makes more appropriate customer segmentation using a lot of data such as customer demographics, information of overdraft, client transactions, contracts, collaterals, customer voice archives to classify customers into microsegments for more targeted interventions.

By using advanced analytics and applying machine-learning algorithms, banks can move to a deeper, more nuanced understanding of their at-risk customers.

Banks moving to an analytics-based model for collections have begun to realize gains in efficiency and effectiveness. A leading North American bank has rolled out several machine learning models that improve the estimation of customer risk, identifying customer with a higher propensity to self-care. These models have so far enabled the banks to save $ 25 million on a $1 billion portfolio.

Most banks can achieve results of this magnitude by

introducing an analytics-based solution quickly and then making the needed

improvement.

Why Futurism Technologies:

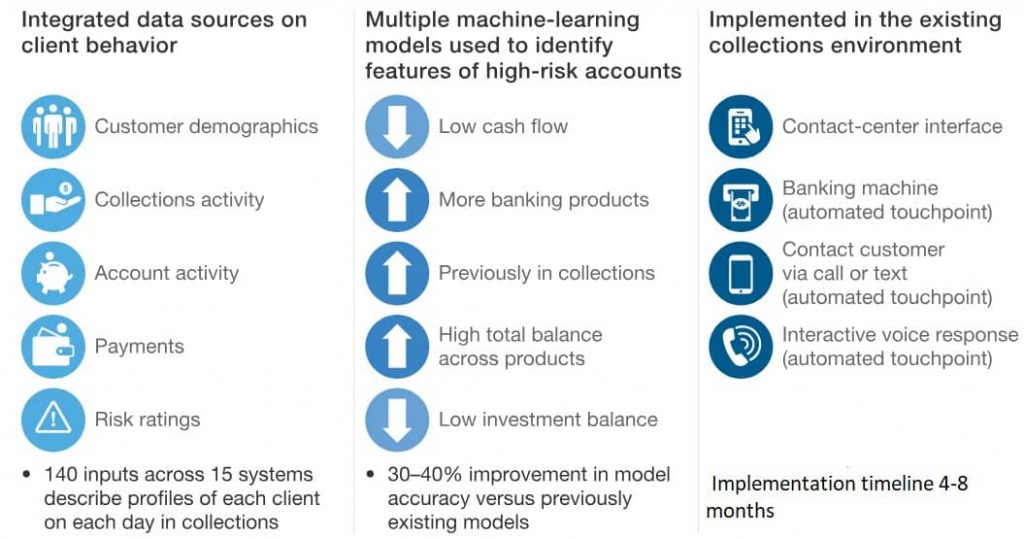

Data science (Machine learning and Artificial Intelligence) requires masses of data from many kinds of sources as a start in the journey to build models to arrive at intelligent business decisions. Data sources include customer demographics, collections and account activity, and risk ratings. Creating a synthetic variable from raw data helps further in enriching the data.

The machine learning or AI (models) built on this data helps identify markers for high-risk accounts from variables such as cash flow status, ownership of banking products, collection history, and banking and investment balances.

Making sense of data is essentially a journey. We at Futurism technologies work along with the customer with a complete team of data scientists, data engineers, testers and banking industry specialists to develop, operationalize and activate (DOA) models to cater to the business needs.

Futurism technologies has worked with multiple customers to implement intelligent debt management solutions using the DOA process framework.

The solution built helped issuers identify the optimal treatment and contact strategy for each delinquent account, deploying the solution inside the existing collections workflow environment, and training collectors to use the system and collect additional data to improve model performance. The rough timeline was about 4- 8 months can vary depending on the maturity and complexity of the data source and models.

Digging Deeper:

Most work today falls into two sides of collections and bad debt management:

● Reactive collections: Using predictive analytics to determine the best efforts for collections. The aim is to prioritize collection activities by ranking those most likely to pay as well as successful outcomes.

● Proactive collections: Pre-delinquency management to identify the triggers and events that take place before someone starts missing out payments so that business can proactively communicate to those customers and keep them on the path away from delinquency

Our approach for most customers has been to look at pre-delinquency management, and this is why we marry the analytics processes with customer engagement. It is about getting to the customer ahead of time and ensuring the right and prompt messaging through the right channels. The predictive analytics drops a lot of past approaches around ranking, segments, and profiling to predict successful outcomes such as customer most likely to pay because of a phone call or a letter. It allows banks to start prioritizing offers and understand if the customer needs a different kind of conversation.

As one size doesn’t fit all, customer segmentation enables us to find an effective approach.

The most significant barrier to analytic success revolves around data, such as having the right data and data connection, methods to manage a large amount of data. Beyond the data some other common challenges include

● People: Being able to attract and retain the right types of people and the right skill sets to keep up with an organization’s analytic demands.

● Tools: Being able to turn all that data into actual insights and into real information that can be used by the business

● Actions: The ability to act on that data. It’s not going to solve any problems having great models and insights if there’s no way to deploy them into business processes and into the channels that involve customer engagement to influence and change behaviors

With these challenges also come opportunities. With data, the question here is can you get at it? What can you access? It might be operational data, billing data, maybe transactional or usage data as well. And that might exist in many different types of systems. As far as people go, again, it’s a matter of skills and volume of resources. Tools are all around bringing in the right technologies that enable efficiency and enable the processes to get us from point A, which is data, to point B, which is process change and insights. And finally, the action piece is making sure that the analytics that you’re chasing is the analytics that is going to solve the business needs and can be used within the processes that exist today for customer engagement.

Bringing all the pieces together will realize in a robust customer view that will enable a lot of analytic insight.

Contact Strategies and Channel Integrations:

The analytics engine built for intelligent debt managed needs to integrate with digital channels. Note that digital channel provides great opportunity to efficiently understand customer behavior and improve risk management even further. One such way is Augmented Analytics, a branch that enables you to learn customer behavior and improve risk management. Integrating augmented analytics with end-to-end CRM analytics is generally the utopian state for many lending houses.

However, the truth is, augmented analytics is a next-generation data and analytics paradigm that uses machine learning to automate data preparation, insight discovery and insight sharing for a broad range of business users, operational workers.

Some of the standard channel integrations are –

1) Websites, Mobile apps – Display messages and repayment options as soon as customers log in to increase awareness and provide opportunities for early delinquency reduction. Web site integration with CRM Analytics gives an added advantage of tracking the effectiveness of messages.

2) Messenger and Chat – Collectors contact customers and negotiate payment options with chat functionality and free messenger applications. Integrating deep learning voice and text analysis helps in understanding customer behavior.

3) Virtual Agents – By calling customers in early delinquency stages, the state-of-the-art virtual collection agent can emulate the best collection agent.

Most banks today understand that analytics and automation will transform their collection operations. Even if there is a reluctance to move ahead, we help the customer to understand and realize the true value of analytics and automation. We explain them logically the power of data analytics in meeting the new delinquency challenges that are on the horizon.

Engagement Model

Every bank can be at a different maturity level of data, process, and people. Futurism Technologies starts with a 2-3 weeks discovery workshop to analyze the readiness of data system, processes, and business goal to charter a program.

In A Nutshell:

Through carefully considering and adopting good predictive analytics and customer engagement practices, banks can reduce their bad debt and improve customer satisfaction. Since each bank faces unique circumstances, the process may vary between companies. That’s precisely why it’s important to consider the individual needs before moving forward.

At Futurism Technologies, we believe that Improving collection operation efficiency and reducing losses is a journey. And with all our knowhows, we will walk with you throughout that journey from data to models, to state-of-the-art pre-delinquency management.

Data Science in Strengthening Debt Management Processes

Subscribe Now!

TRENDING POSTS

-

AI Personalization ROI: The $500M Opportunity for Enterprises

-

Zero-Click Marketing: Why Enterprises Must Rethink Attribution in the Digital Age

-

Agentic AI and Generative AI: What’s Best for Your Business?

-

Deepfake Scams: How to Protect Your Business in the Age of AI

-

AI and Cybersecurity: A Strategic Guide for C-Suite Leaders in 2025

-

How Location Intelligence is Revolutionizing BFSI: 6 Must-Know Benefits

-

Cloud and Data Engineering: The Path to Faster Insights and Smarter Decisions

-

From Delays to Innovation: How AI is Optimizing the Construction Industry

-

Data-Driven Future: 6 Trends to Watch Out For

-

The Impact of IoT on Reducing Maritime Carbon Footprints

-

Demystifying SASE: What is Secure Access Service Edge?

-

The Role of AI in Construction Safety

-

What Is Predictive Maintenance and Why Does It Matter?

-

What is Ransomware-as-a-Service (RaaS)? Everything You Need To Know

-

The Role of Smart Maritime IoT Solutions in Enhancing Maritime Safety

-

Revolutionizing Telecom with AI-Driven Network Slicing

-

Data Integration Unlocked: From Silos to Strategy for Competitive Success

-

Navigating the Shadows: Understanding Zero-Click Attacks in the Digital Age

-

AI Reimagined: Crafting Next-Gen AI Apps with Expert Fine-Tuning

-

Futurism AI: Turning Ideas into Apps at Lightning-Fast Speed

-

Accelerate AI Across Your Enterprise With Futurism AI

-

Flying into the Future: How AI is Redefining the Future of Aviation

-

Beyond Intelligence: The Rise of Self-Healing AI

-

The Indispensable Role of a Trusted Offshore AI Company in 2024 & Beyond

-

IoT-Powered Smart Warehouse Management: A Detailed Guide

-

Turning Data into Dollars: The Futurism Path to AI-Driven Success

-

5 Ways to Prepare Your Business for Digital Transformation

-

4 Ways To Win at Digital Transformation on a Shoestring Budget

-

Why AI in Digital Marketing is the Next Big Thing?

-

How AI Will Enable Faster Adaptation of Digital Transformation

-

How Is Digital Modernization Important In Supplier On-Boarding?

-

Top 10 Email Marketing Tips for This Holiday Season

-

Benefits of using ERP Software for Energy and Gas Industries

-

5 Features of Supply Chain Management Software